Lessons of 2021 - Stocks

Lessons of 2021 - Stocks

My reflections and learnings across Stocks in 2021.

Quarterly reflections of 2021

My first article on Substack was on February, but I will summarize the reflections by quarters as many of the lessons have slight overlaps. Let’s dive in.

Stocks

I’d rather not give a boring paragraph on how I got into stocks investing. Rather, if you’re reading this, you should know the importance of stocks and its ability to help you reach your financial goals faster than your job ever could.

This applies similarly to crypto, but there’s only one person standing in the way of you and your investing success - you. I’ll be very honest and say that it’s not the stock-picking that is tough. It’s how you respond to what Mr Market doles out to you.

I am still a young investor, having started (on serious terms) in Feb 2020. I experienced quite the mother of manic-bull markets. Markets don’t go up in a straight line. Bear markets will come. Your behavior will either buy you your dip in a long-term secular uptrend, or panic sell your precious stocks after a 40% drawdown.

Reflection is something that I feel is sorely missing from many investors’ toolkit. Only by reflecting will we make ourselves a better person and investors.

My articles here:

Q1 2021 - Stocks

Funny that the second sentence I wrote in the Feb article was about inflation. 😆

Next came the rise in bond yields stoking fears of inflation going out of whack, despite the Fed being absolutely prepared to manage this if it goes awry.

I’ve learnt and grown so much since then, but yet inflation is still at the top of mind - then and now. Some narratives never change.

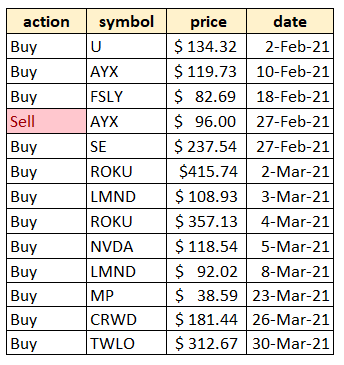

February was quite brutal for investors of high growth stocks (especially of the SaaS kind), though for experienced investors, it would be par for the course. Prices don’t rocket up 2, 3, 4x from Covid lows and suddenly for a base there for further multiple expansion. I was not entertaining thoughts on sky-high valuations/multiples for sure. In March, the correction (for the faint of heart, it was a bear market) ensued. I tried my best to buy the dip. My full purchases (and sales) below.

With the benefit of hindsight, only $U $NVDA $MP $CRWD was higher than where I bought it at. These are all in the past. Nothing I can do to change it. What (if any) was the mistake or the lesson here? In my opinion it is this:

The higher the current expected return, the lower the future expected returns.

I was nowhere near incorporating valuations of my companies in my investment management. I thought, this time will be different, and that COVID did indeed permanently alter the nature & prospect of companies which I own. That should deserve a higher multiple, right? Furthermore, if I held on for the long-term, I would be in profit yes? In March my buys were likely fueled more due to % day returns. Sometimes markets would correct and my growth stocks (which were high beta and express higher volatility than market indices) would correct even further.

Wow, a -10% in the day (!) is quite a good opportunity, no?

Narrator: It was not.

The lesson here is quite simple, but really hard to internalize. Prioritize multiples or bottom lines and you will miss mega winners over the past 10 years (e.g. $NFLX which only turned cash-flow positive recently). However, being greedy just as others are equally greedy (like in bull markets) will not always lead to an optimal outcome.

Investing is hard.

Where will the incremental buyers come from? If continually DCA-ing into your favorite stocks every month, I think you can afford to be less stringent with timing. For me, I still have to incur transaction fees per order + no fractional share purchases (not on the platform I’m on). I am tightening my investment contributions too due to life commitments. Hence, I have to be timing the market one way or another.

People will disagree with me and say that time in the market > timing the market. I agree. That is why I am currently only < 10% in cash. Perhaps the cash in my account serves a more spiritual purpose than just buying the dip.

Always have cash on the sidelines.

My articles here:

Q2 2021 - Stocks

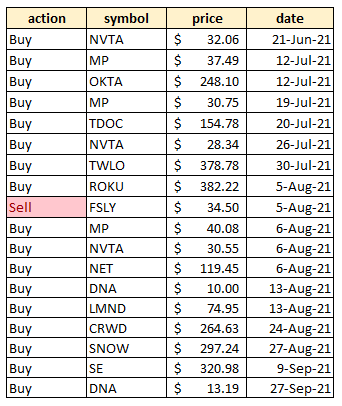

My purchases during this quarter are below.

I also had this quote in the April 2021 article.

When things are going well and prices are high, investors rush to buy, forgetting all prudence. Then, when there’s chaos all around and assets are on the bargain counter, they lose all willingness to bear risk and rush to sell. And it will ever be so.

(Chapter 9) Uncommon Sense for the thoughtful investor by Howard Marks

I think I deserve to re-read this once in awhile. Good prices on $DDOG and $NVDA though. Shows many things but that you can’t predict the future, or that winners will keep winning. 6 months isn’t nearly as long for company fundamentals to align with price. Of the stocks that are in the red for my buys, I’ve only sold off $NVTA. Meanwhile, $TDOC and $TWLO is still growing >50% in revenue y/y. Metrics are pointing in the right direction, company seems to be executing.

I italicized the word seems because if everybody can tell definitively that the company is executing, that would be classified as a winner. But yet, we also know that outperformance only happens to the right tail of the universe of companies. We also know that perhaps 80-90% of investors underperform the market (left tail) over the long term. This means that the company you think is executing may end up being a loser over time. What do?

Investing is hard.

Generally speaking, the longer the company has been executing ($NVDA), the more likely a winner the company will become and consequently the lesser returns this company will get (because you only bought after it becomes a winner). The earlier you buy a company stock that has yet to execute, the chances of it being a winner is of course, lower.

And here we are trying to own companies in hopes of it becoming blue-chips (or FAANG) of the 2020s.

Bring it on, Mr Market!

I also talked about how the human element is oh so important in investing (and in life really). The greatest opponent is always yourself. We trust ourselves to behave optimally in times of opportunity, yet we somehow seem to flunk it every time it materializes. The only way to rectify this habit is by creating a new one.

Identify what you did wrong. This can only happen by active reflection. Do you avoid your mistakes? Or do you face and review them? Do you review them in your head? Or do you document them down? What are the next steps?

Is there a plan for you to do the correct thing when the time comes? Is the plan documented down, or is it in your head? If the latter, are you making sure (without doubt) that the next time such an opportunity arises, you will grab it by the balls (with certainty)?

We are our own greatest rival and our worst enemy.

Another plug to read Thinking Fast and Slow by Daniel Kahneman. Understanding just how much biases we have in our lives is easily the greatest revelation I’ve had in recent years.

The last point I talked about was intrinsic value. I won’t rehash the whole topic here. Suffice to say that we all form our own opinions of the company’s intrinsic value. They can be right or wrong. You can come from a user perspective and having tried a company’s product, arrive to the same conclusion another analyst did with his 10-tab excel VBA-enabled discounted cash flow model.

Of course, there are proven guideposts that can measure a company’s intrinsic value to a certain extent such as user growth, product development etc. Over this half a year, I managed to solidify my framework for tracking metrics framework for all my portfolio companies.

This allows me to validate the direction of execution (good, great, not so good or bad). Once this is more or less certain (after corroboration with smarter investors on my Twitter list), then what remains is valuation and your cash position. You only need to worry about valuation (which isn’t really a concern if investing for > 5 years) and cash position. These solve themselves pretty quickly. If price goes too far ahead of itself, don’t buy. Else, if you’ve got ample cash, buy.

Though, investing isn’t that easy, is it?

In case I lost you, the key lessons:

Intrinsic value can be tracked (direction rather than precise magnitude). Price can diverge strongly from this value. If investing for long-term, valuation is less of a priority.

You get the returns you deserve since YOU make the decisions. YOUR decisions will make you poor or wealthy. The world can be unfair but what’s important is YOUR response to that.

My articles here:

Q3 2021 - Stocks

Note that I’ve already sold off $NVTA and $DNA. Funny how things work when reflecting on my previous buys. I documented each and every sale/purchase as well as some comments as to why I bought it. If I were to do text mining on these remarks, it would likely be a 40/40/20 split between FOMO, Earnings-related and others.

It isn’t easy to remove the feeling of FOMO in your investment decision making. After 20 months of investing, I think I still give in to FOMO sometimes. It is perhaps a consequence of curating a list of accounts with high signal-to-noise ratio; you tend to be influenced by their moves as well. It’s not an easy trap to avoid.

As mentioned in the earlier sections, you are your greatest adversary. You are also your greatest benefactor. The accounts (whom which you are influenced by) don’t know that you made your decision partly (or wholly) because of them. They don’t care.

That is something I must work on. The only way to eliminate the FOMO is to have a plan (and execute on it).

Personally though, I think being influenced by other investors on FinTwit is not all that bad. Especially when these investors are more experienced and have provably better domain knowledge (in say cybersecurity). However, it’s up to YOU to make sense of their words. You don’t have to agree with them 100% of the time. The words THEY say will feed into YOUR mental model one way or another.

FOMO is a direct consequence of having an unfiltered mental model, like an all-powerful Dyson vacuum V12. Your mental model is the amalgamation of all things, rubbish or not. That’s FOMO. How do we avoid it?

We need to ground our mental model in hypotheses. Something that can be proven (or disproven) irrefutably. My mental model for stocks is a simple one.

I read through the company’s description in their 10-K or 10-Q to understand what the company is about. This is compared against my worldview (e.g. do I think it is a trend/narrative worth investing in).

I then summarize my own personal investment thesis of that company. This can come from already published research written by Muji@hhhypergrowth.

I start compiling company metrics (see pic), though depending on the company chosen, there's no real need to compile 8 quarters back, though you should, if you want a sensing of how the company was like pre-COVID.

For each subsequent earnings call, I summarize my thoughts on their results in a separate word doc and post a more concise version on Twitter. Concurrently, I also read what other investors post about the earnings.

The mental model is quite straight forward. Here you can see that the outside influence (aka FinTwit) acts as confluence only in point 3 (and 2) to help me form a more robust viewpoint on the company itself. That is my mental model. To each its own. Just remember to form YOUR own opinions about the stock. Because when shit hits the fan, YOUR decision counts. Not theirs’. YOU are what’s important. Not them.

My articles here:

Q4 2021 - Stocks

Having read the articles in Q4, I think they are largely centered around the same lessons gleaned in Q1 to Q3. I think I observed a slight obsession for me to blabber on in my Substack articles, so will keep this short (hopefully).

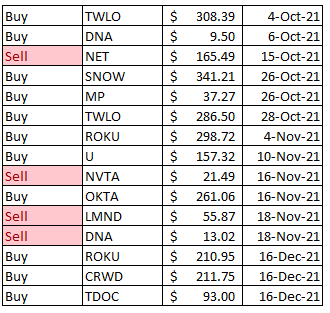

My position changes in Q4:

Note that amount is hidden, and just to reiterate, I’ve completely sold of $NVTA, $LMND and $DNA. The proceeds were used to buy $ROKU, $CRWD and $TDOC, as well as other limit orders for $SNOW, $U and $NET. Potentially, $TSLA but having dipped too $880+ it’s safe to say I’ve missed my train.

Perhaps if there’s one lesson here, it is the importance of having a structured framework for portfolio management. I don’t really manage my portfolio under clear rules and structured guidelines. The overarching message on the board is buy good companies and hold them for the long term.

Thinking about this, it’s like asking a captain of a ship to reflect on his travels, when he’s only been told to go to the end of the world.

Whilst keeping track of my purchases and sales (+ added commentary as to rationale behind purchase) is a good start, it is nowhere near a functioning strategy, no? All the talk about me being my own obstacle to success above and here I am being biased and thinking my discretionary management skills will somehow lead me to become the next warren buffet.

I think this is something that I will try to integrate in my overall strategy. For example, what is my hurdle rate for selling one company for another? When should I sell a company? By what metric should we define a bad quarter? How much should I allocate to my best idea (holding)? Should I incorporate hedging in my strategy?

These are still questions I have not found answers to in 2021. Perhaps 2022 will be better?

Conclusion

Thank you all for reading thus far. This article is a special edition of my monthly portfolio review as I wanted to document and summarize the learnings and reflect upon my decisions for 2021.

My investment objective is simply to achieve outsized returns over the long-term. Obviously, it’s not that simple to achieve. The key thing is to continuously reiterate and put in effort such that you auto-compound your knowledge and good habits.

In doing so, you multiple the good habits (decisions) by 1.01, and the bad habits (decisions) by 0.99. Over time, one will trend to infinity, and the other to 0. The outcome of your investing should follow proportionately.

You only got one life, folks.

Good things come to those who wait. Great things come to those who hustle.

Cheers,

Joey