Equities Portfolio breakdown

Note:

% of portfolio uses market value.

Cost allocation denotes my cost basis as a % of full position size. 100% means it is a full position, whereas 100% + denotes an overweight position.

% cost represents the cost basis as a % of my total $ invested in portfolio.

Equities Portfolio Performance

Portfolio Changes

Bought: ROKU, MP, NVTA, NET, LMND, CWRD

Started: SRNG (DNA), SNOW (more on why in next month’s writeup!)

Sold: $FSLY

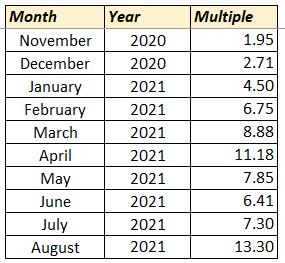

Crypto Portfolio Performance*

*Multiple is expressed as: Total crypto assets ($)/ Total $ cost into crypto. The last time I added real-life money into crypto was in July 2020, so my starting point (to be conservative) will be Jan 2020. Portfolio breakdown is shown below in the Crypto section.

% of Net Worth (exclude house/car) in:

Stocks: 19%

Crypto: 77% (not by choice!)

Equities Portfolio commentary

The momentum of growth stocks waned from the fever in May/June and Jan/Feb, resulting in what I would call market chop for most companies in my portfolio. It’s surely not a bull run, and perhaps investors were taking stock of what they actually own after 1.5 years of money printer go brrrrr. Add to that the massive china crackdown on select sectors spilling over to US stocks, and the occassional market fear of a earlier-than-expected taper tantrum, and we’ve got legitimate bear porn. Jerome Powell still holds the key to the vault though, and as his speech (on friday) has shown, markets (both equities and crypto) loved it.

What does these all tell you? Sometimes it’s better to simply zoom out and focus on owning the best companies for the longest time possible. The stock market will do what it will do. Not an easy task, but I’ve managed to distract myself from it by writing threads :) Keep a lookout for them on my profile (mostly crypto though).

On a serious note though, the last thing you should do is to fret over your portfolio drawdowns. Why? Your portfolio is simply, the sum of its parts. Assuming you’re investing in individual stocks, you need to at least have a decent understanding of why other investors will pay money at increasingly higher price points for your company. Something like “this company is good” isn’t going to cut it. The least you could do is to be able to sell (convince) it. For example, how can you sell a company like Sea Limited to convince your friends to buy it? We can take reference to my thread on its Q2 earnings:

This company is the regional leader (South East Asia) in 2 fronts: Mobile gaming & E-commerce. On gaming, it’s the highest grossing mobile game in the world: SEA & Latin America (8th straight Q), India (3rd straight Q). Leadership in developing region (SEA/LATAM) means it’s no 1-game wonder; It is ranked 3rd globally by average monthly active users (MAU) on Google Play.

On E-commerce: Shopee app is the 2nd most downloaded in shopping category for both app stores. Top mobile app by average MAU in SEA/Brazil. Malaysia became 2nd market to go adjusted (earnings) EBIDTA positive after Taiwan, showing increased monetization. Overall, on global basis, average buy per user per month is about 6x (!). This means Shopee users on average buy from Shopee 6 times a month.

Putting 2 and 2 together, we can see a company dominating in developing regions (LATAM/SEA), and are top contenders to capture the mindshare of global consumers with key social apps (gaming, shopping).

It’s surely far from perfect, but I am very comfortable investing in a proven leader that is executing on 2 fronts (have omitted SeaMoney which is also at hypergrowth stage, but still has more to prove).

Nobody said individual stock investing was easy, and those who choose this path need to be upfront with your own self. The least you can do is to be familiar with the companies you’re investing in. Sure, sometimes a company like cloudflare ($NET) will be hard to understand and to sell (they operate in the network infrastructure + security space), but at least, we should be able to sell some metrics, such as their revenue, customer base, retention rates, to let the numbers speak for itself. Remember, you’re investing in a company to help you invest and grow your capital. Don’t ruin the power of compounding by just blindly following others into a stock you barely know!

If you decide not to play this game, ETFs are always a strong alternative. What’s more, you can take pleasure in knowing that 80% of investors underperform the market 😂.

I choose to play the hard game, and in doing so, I will put in more effort than others. Will you?

Earnings Season

The month of August was finally upon us, which meant that most of my companies released their earnings. It was exciting because it’s one of the 4 times in a year where you can validate your thesis on the companies that you invest in. I usually start by skimming through the earnings call transcript (which is usually the whole thing), then re-reading & summarizing it in a word doc (max 1 page). Then, I write a Twitter thread on their earnings. This thread is collated with other threads on my portfolio companies into a meta-thread for that quarter, which you can find here, or in the links below. I felt my Twitter threads where quite concise, and so I won’t summarise them further here.

Invitae, Teladoc, Roku, Twilio, MP Materials, Fastly (closed), Lemonade, Cloudflare, Datadog, Unity, Sea Limited, Nvidia

As Fastly was kicked out of my portfolio, it deserved a separate section on its own.

Fastly

I sold Fastly after their Q2 2021 earnings where they lost (temporarily) another big customer (FinTwit says its Amazon) who’s currently diverting their traffic in-house and waiting to see remediation steps being taken (by Fastly) before shifting the traffic back. In light of this, management lowered guidance, while attempting to reassure the analysts that the company is still directionally in a tailwind and that “it will all be OK in 2022”.

There was an ever-present aura of hope I felt in Fastly. Hope is often not a good thing (especially in investing). We shouldn’t hope the company does well; there should (and will) be evidence of it (shown in operating metrics and earnings call). That said, I was lured in by its usage-based growth from Tik-Tok (TT) who then left Fastly from Akamai 😥. The next hope was Compute@Edge, but from its limited availability in end 2020 till management’s repeated calls for (it’ll all be OK) 2022, there was too much hoping. There was other reasons why I sold of course, but the core mistake I made was that I hoped. Hope doesn’t bring you your outsized returns. Imagination is necessary to see the company’s potential 5 to 10 years out, but hope is never needed. Your investing thesis should be continually verified; If time after time the thesis was invalidated, it is time to let it go. If you’re interested, you can find my threadon Fastly’s earnings here.

Reading list

Howard mark’s second memo of the year, in which he writes about how macro forecasters more often than not, gets it wrong, and that macro forecasts (as in how far/long inflation is going to run heated) are akin to a coin toss. However, this does not mean inflation isn’t here, nor that infation will always be here. Rather, it is to remove inflation (or other macro forecasts like interest rates) from your investment decisions, and that to make short-term decisions (trimming / selling) on a long-term vehicle (your investments) would not be the wisest choices. We will never know when the time is right for the Fed to taper or to raise interest rates. Even the Fed don’t know it themselves.

Beth Kingdig’s excellent podcast talks about trends, microtrends, current valuations and many more growth stocks. She was one of the first people on FinTwit bullish on Roku, as well as Nvidia, as well as being bearish on Fastly’s execution. That should tell you how cognizant she is of current and future trends and how strong (or weak) companies fit into such trends and tailwinds. Likewise, investors in growth stock must really understand the underlying trends (EVs, Edge Computing, ; is it a super strong company with a dying trend? Or is it a company in a super trend that takes perhaps a few more years to materialize?

Mattthew’s essay on the 7 reasons why gaming will take over: (1) what gaming competes against; (2) how it’s (now) being packaged; (3) why it’s such a uniquely scalable medium; (4) why people play today and will play more in the future; (5) why it’s such an engaging medium overall; (6) the unique growth potential in the medium; and (7) why it’s the modern comicbook. Particularly relevant when you see Netflix producing games in the future. They know where the money (and potential) is! While a dated article (Jan 2020), many of the points hold true in August of 2021. Investors may do very well over the next decade to sieve out the key players in such a tailwind that are investible.

Arthur’s article on how individuals will flex social superiority in the metaverse. This is a timely article considering we’ve had CEOs of Facebook, Unity and Nvidia (and more) actively working on making the metaverse a reality. While we don’t know what and how it will take shape, we know it will definitely be digitally native. The article draws stark similaries between how we as humans flex (consciously or unconsciously) on other humans in reality vs the digital world (internet). The former does so via flex goods ranging from physical art to collectibles to hype wear and the like. The latter does so via pet rocks, punks, kitties and even penguins. It’s something I think people not exposed to crypto can definitely relate to and hence it’s worth the read.

The generalist’s trilogy on FTX, the up and coming cryptocurrency exchange (built for traders, by traders) taking the world by storm. I’ve been a longtime crypto investor and FTX for me was the exchange that blew me away. Their user interface, experience were such a delight. This is a company that went from a small exchange to one with 18B valuation in just 2 years. Their H1 volume was 1.875 trillion (!) while Coinbase’s was 0.797 trillion. FTX’s revenue of ~400 million compares with coinbase’s 3.63 billion. Take rates for Coinbase = 0.46% while FTX = 0.021%. This shows the revenue that coinbase earns from trading volumes (i.e. fees) are at around 23x higher. For my crypto activities, FTX is my crypto exchange of choice. Here are the links to part 1, part 2 and part 3.

Crypto

Bitcoin and other crypto has been surprisingly resilient ever since the endless FUD from governments claiming to ban or to regulate crypto. They want to do lots of naughty things to crypto, and yet BTC is now close to 50K. As it stands, it seems like crypto as an asset class has marked a short-term bottom supporting the price momentum. Many large-cap altcoins have broken through their ATH (like ADA/SOL) and then some.

As a longtime holder who has now experienced 2 bear cycles (2018-2019, May-July 2021), I am certain that bull and bear market cycles will happen even quicker now with widespread access to crypto. Crypto just had its bull market from end-2020 till May 2021, a bear market from May to July 2021, then now another bull market in August 2021. Where else can you experience market cycles in under a year?

Despite it being a nascent asset class, its clear money and capital is flowing into it. This represents an opportunity that can be capitalized on. Furthermore, the crypto bull cycle has been really kind to me. As such, it makes sense that I allocate more time and effort based on my net worth. I’ll also start a more formal commentary on crypto every month to post updates on crypto world (DeFi etc.) for transperancy. Do note that my strategies are not for everybody, so please don’t try and replicate what I do. Act on your own risk appetite and tolerance.

Where to start?

For now, I’ve managed to organize the threads and content I’ve read across crypto categories into 3 meta-threads. If you’re interested in the space, you may wish to start there :)

I have also written simple threads on crypto 101, focusing on terminology that investors new to crypto may have trouble understanding. This will be collated into a meta-thread that you can see below.

[You can follow me here to receive running updates on these threads as I write them.]

My portfolio composition (ultra-speculative bags are denoted as others) can be seen below (as % of current value):

Compass Mining denotes cash paid to procure miners for BTC mining (not started mining yet & hence no depreciation). To say I’m bullish on the Solana ecosystem may be an understatement.

Yield Farming

You can refer to this simple guide for what yield farming is all about. I may also write a thread on it in the future, so do keep a lookout on my profile by following me if you haven’t already! Generally, of the tokens I own, these are the DeFi protocols that I am putting money with. I write a running thread to organize all my own DeFi developments here (or search for #joeythedefipleb).

Disclaimer: As a reminder, yields are often rewarded in their native token which is usually used for governance. To protect yourself against price risk (i.e. native token (in this case SBR or MER or CHESS or XAVA) dropping in price, you may want to sell the native tokens to USD tokens on a daily basis or short their derivative contracts on an exchange to preserve Delta-neutrality).

[Solana] Saber

Saber is a automated market maker (AMM) protocol that focuses on providing liquidity on cross-chain assets. It’s similar to other DeFi protocols that reward users for providing liquidity, except it differs on the types of tokes it is providing liquidity for. With Wormhole providing a bridge from ecosystems like ETH, any assets sent across sent across chains have to be wrapped in the base protocol’s clothes (like formats, code for compatibility). As an example, a wrapped Ethereum on Solana would likely be wETH. As such, the AMM provides liquidity for swaps like FTT/wFTT.

Barring unforeseen circumstances with the prices of such pegged assets, there is little risk of an impermanent loss as we’ve seen on other token-USDC pools. It’s kind of like putting your spot coins to work without having to convert to another token like USDC which isn’t correlated to the other side of the pool. Of my tokens in DeFi, this is where most of it is.

Yields are low mainly because of the emissions curve of native tokens, the total amount staked, as well as the dollar value of such tokens (which will be used to derived the APY).

[Binance Smart Chain] Tranchess

Tranchess is a tokenized asset management and derivatives trading protocol. Inspired by tranche funds’ ability to satisfy users’ varying risk appetites, Tranchess aims to provide a different risk/return matrix out of a single main fund that tracks a specific underlying asset (e.g. BTC). Simply put, there are 3 ways (tokens) to put your money to work on Tranchess:

Queen: A single share in a BTCB (Pegged Bitcoin on Binance Smart Chain) tracking index fund. It’s an synthetic ETF.

BISHOP: Holders earn interest from ROOK holders paying them (see below).

ROOK: A leveraged product with no forced liquidation. The ROOK holder borrows daily from BISHOP holder to buy the main fund tracking BTC. ROOK receives all gains/losses associated with BTC less interest paid to BISHOP. By borrowing from BISHOP, ROOK can increase leverage to juice returns.

I currently have funds in the BISHOP tranche, which is earning around >70% APY.

[Avalanche]

After enjoying the last moments of their AVAX-XAVA farm with > 80% yield, I shifted my funds to single-sided staking pools on beaten-down tokesn like XAVA and JOE, both of which offers >40% APY. This also maintains my long exposure in those coins, which I’m happy to have. The funds are now deposited in a auto-compound farming protocol on Avalanche, YieldYak.

NOTE: Do note volatility works both ways in crypto, and in a bear market these yields will significantly depress as the prices of native tokens that are emitted as yield will also crash (see original disclaimer above).

If you are interested in yield farming, you may want to take a look at their emissions protocol, as yields tend to be very high in the first periods of the protocol’s birth as they reward early participants.

As always, the risk of cryptocurrencies are generally higher, as are the risk of exploitation or rugging is way higher too. This is NOT financial advice. DYOR!

In terms of other cryptocurrency activities, I am more focused on the solana (for NFTs as well) and avalanche (to a lesser extent).

Bitcoin Mining

My last section will focus on Bitcoin mining. There is nothing much to update, as the miners I’ve bought is not yet operational. I have already done up a fancy excel table projecting costs and expected revenues, but can only record it until the miners come online. I have 2 miners coming online: End-Sept (1) and End-Oct (1). Will share it on my Oct substack onwards!

I’ve outlined my reasoning behind buying these miners here (CTRL + F for mining). The resources are there as well, but I’ll share the link here again. Will continue encouraging people interesting in having exposure to crypto (with stable-r gains) to simply purchase a miner. With that, you can truly experience how bitcoin is actually used, and understand the true promise of Satoshi’s vision. Comprehensive article form someone with skin in the game here.

Conclusion

Thank you for reading thus far. Having spent most of this month reading and collating info on Crypto/NFT/Solana as well as writing educational crypto threads, I have rediscovered the wonders of sharing and simply spreading my knowledge on Twitter.

I hope to continue writing further, perhaps lowering the barriers to entry for the average user to learn and invest in crypto :)

Stay safe, and compound 👍

Joey