Portfolio Review - Mar 2023

Portfolio Review - Mar 2023

March came with a bang! (or bank!)

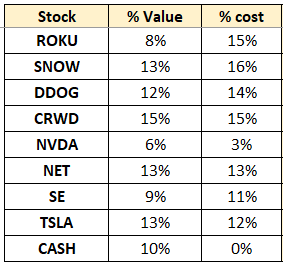

Equity Portfolio Breakdown

% Value: Value as % of my portfolio

% Cost: Cost as a % of my total cost invested into equities

This table simply visualises the divergence between my investment thesis and the current market expectations of the company. No hard rule on % cost allocation for stocks yet, nor a threshold where I will trim them.

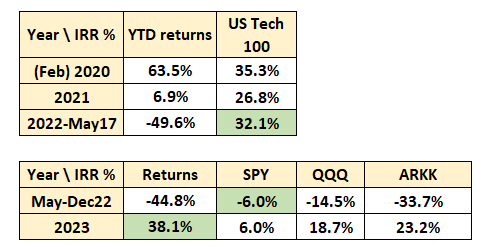

Equity Portfolio Performance

Historical Portfolio Returns (top); Cumulative Portfolio Returns (bottom) - Since new brokerage.

Monthly Portfolio Returns

CAGR Performance

Note: CAGR for my portfolio is calculated as:

(market value of portfolio including cash / total cost) - 1

The CAGR returns are compared in the above table instead.

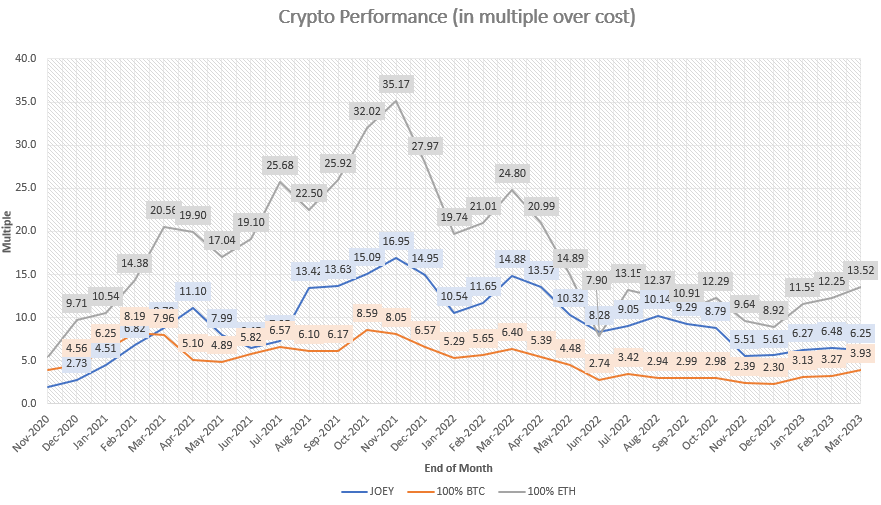

Crypto Portfolio Performance

* Charts start from end of November 2020 when I started recording my crypto portfolio. Summarizing:

2020 performance: 2.7x-ed my portfolio

2021 performance: 5.5x-ed my 2020 portfolio

Lifetime performance: 6.25x my cost

Lifetime result:

- Achieved 1.59x of BTC performance (6.25/3.93)

- Achieved 0.46x of ETH performance (6.25/13.52)

When all you had to do is to be in BTC or ETH… but not me, a clown. Very hard to keep pace with the majors.

Net worth growth

If there’s only one metric that you can apply to your financial life, I believe that would be net worth. If you’re investing, perhaps under 5% of your gross income for investments, it’s a little hard (compounding considered) to eventually make a dent in your net worth.

To read this chart:

I’ve received ~20x my Jul 2019 net worth, in terms of income / bonus.

I’ve made my money work, and my net worth now is ~19.5x my Jul 2019 net worth.

I’ve accumulated savings of 7x my Jul 2019 net worth.

Red line is an extreme example; Anywhere between grey and red is acceptable, since you’re supposed to compound your savings, and not your income (i.e. you don’t spend anything). Onwards and upwards!

Thank you for reading my monthly journal of my portfolio. I keep it very real and authentic because nobody can buy the bottom and sell the top. Life is full of mistakes and writing this helps me identify what went wrong and how I can improve. Besides investment I also talk about my life (also a journey) as I live through it.

Catch the monthly update of my personal and investing life by subscribing below.

Equities portfolio review

Portfolio movements

Buys: TSLA 2x, CRWD 3x, DDOG, SNOW, ROKU, SE, NET

March madness came with a bank! (pun intended), with me deploying most of my spare capital (from my TSLA and NVDA sells last month. I had a very strong hunch and Mar 2020 vibes, so I struck while the iron was hot. For my passive investoors, let me bring you up to speed.

Sells: NVDA

I wanted to get more cash (to buy dips), and given that Jim Cramer tweeted positively about Nvidia near its historical highs, I sold another tranche. I think that it is already richly valued, and so not very optimistic about forward returns at that price. Still have a final tranche of NVDA which I will sell if price ever gets there (~$28x).

Silicon Valley Bank (SVB)

On Mar 10, the Federal Deposit Insurance Corporation (FDIC; the agency who insures residents’ deposits) shuttered Silicon Valley Bank (SVB), seizing its deposits in the second-largest bank collapse in US history. A good thread explaining it here.

What happened?

SVB was very pro-VC, doling out loans to startups with favorable terms that founders couldn’t get anywhere else. In exchange, startups had to bank with SVB as their primary partner. With deposits, SVB did what most banks do; buying bonds at the prevailing market rate to earn yield above what they pay out to deposits (the net of which is called “net interest margin”).

This virtuous cycle was kickstarted with the bazooka of stimulus payments / money printing from the Fed, which brought us the great bull markets of 2020/2021. With practically 0% interest rates, there wasn’t much of a choice for banks to earn extra yield (compared to the differentials we see now), and so they had to buy. And in large amounts they did.

The final nail in the coffin was that they bought bonds that were considered hold-to-maturity, essentially locking the interest rates for close to 10 years. Fast forward to 2023, interest rates sit at an attractive 5%, while SVB’s bonds/securities were bought for perhaps < 1%.

Bond math => Interest rates go up, bond prices go down.

SVB was sitting on huge unrealised losses, which will be realised if they sold these security, for liquidity reasons (e.g. if people are asking for their deposits back). With the macro-recessionary environment that all but decimated the start-up scene, deposits burned like paper, leading to liquidity concerns for SVB (all their $ was stuck in bonds).

Desperate, they announced a capital raise, which prompted Moody’s to downgrade the company. Rumors of solvency risks spread like wildfire, which prompted SVB depositors to demand for their money enmasse. Even with the sales of bonds (which realised huge losses) of 21b, they weren’t able to make depositors whole (depositors wanted to withdraw 42 billion!). SVB can’t pay, and thus was seized by the government.

Regulators responded eventually over the next week, saying that they’ll make investors whole. The Fed also responded by injecting liquidity back into the markets, allowing the temporary-but-terrifying bank run to subside.

That’s about it; Here’s another article summarising the events.

From that SVB fiasco, the markets got spooked, and the panic reached its highest Monday morning (13th March). From my understanding of the markets and the 2008 crisis (where they did their best to not let banks fail), I had a feeling that the government (specifically the Fed) won’t let SVB fail w/o doing something about it.

And they eventually did, and it resulted in a considerable retrace of the QT done over 2022. Every doom-poster was forewarning in 2022 that something will break after all these interest rate hikes and QT, and I guess they got what they wanted.

Having been sideline in Mar 2020 (where panic was also at its peak), I was determined not to let that happen again. My base case was that my portfolio will continue to bleed, which is normal for bear markets. But, I was confident that Fed will flinch and inject liquidity, sending markets back into up-only mode (for at least a short while until the next Fed meeting).

I deployed close to 80% of my cash into my current portfolio, and I feel pretty great about my monthly performance.

Of course, shortly after, Credit Suisse also started showing some problems with solvency, but that’s probably a Europe issue rather than a US issue, and I’ll spare you the unnecessary details.

Enough distractions; let’s end this section by talking about my reaction towards the earnings for my portfolio holdings.

Earnings

The 3 companies showed strong earnings, each from a different perspective.

Sea Limited

The company that was described as a 3-headed dragon turned to 2 with the ban of Free Fire in India and the normalisation of user trends in the game from the start of 2022. It appears to be seen if they can stop the bleeding and eek out growth in the user base again. For E-commerce, despite a screeching halt on S&M expenses (i.e. promotional for each month, such as the 3.3 buying festival), it managed to turn positive in adjusted EBITDA, which is nothing short of impressive. Can they still maintain market share while optimising these promotional spends? Brazil also looked like that are just 1-2 quarters from achieving breakeven, after which the entire pillar will be generating positive EBITDA, thus freeing itself from the grasps of Free Fire.

The last pillar, SeaMoney, also went positive in adjusted EBITDA, offsetting the bleed from Garena, and still showing strong growth (though management not revealing user metrics is kind of a yellow flag for me). Nonetheless, it’s a company I’m comfortable holding and (slowly) accumulating shares in.

Snowflake

Customers still want to get onboard Snowflake, though instead of multi-year deals or yearly renewals (which bodes well for sales pipelines), they have opted for pay-as-you-go credits, which clouds their ability to forecast the future in terms of guidance for the new FY. Snow Park (i.e. Snowflake for Python) seeing strong adoption, with 20% of customers already trying, with massive cost savings over it’s legacy counterpart (Spark jobs). Not much to complain about besides what I said above; the company is a buy for me as long as its user metrics don’t see significant slowdown.

Crowdstrike

Valuation already out of top 10 SaaS companies, yet its top-line and customer adoption is still best-in-class, with cybersecurity being in huge demand (as ever). Crowdstrike is firing on all cylinders, and even in this slowed environment, is showing no signs of slowing down.

What people don’t understand is that this company shouldn’t be valued like other tech companies, since its product offering is mission critical and literally saves companies (by virtue of them not being vulnerable to attacks / hacks). Their emerging product category is also on fire it seems, and will further throttle top-line growth well into the depths of 2023, wherever it may be.

Company is a buy.

DCA investments

Endowus

With added income from my performance bonus, I added a little more than my usual monthly allocation. Month 3 and this strategy seems to be progressing well - though would love to have prices lower so I can buy more.

URA

Crypto Portfolio Commentary

The SVB crisis did a number on the financial markets, but as it unfolded Crypto Twitter started peddling the narrative that Bitcoin is the ultimate bank hedge (in that it is truly your money). The market believed in it, given that Bittycoin is moving 5%+, almost on a daily basis, since FDIC said it’ll insure SVB and Fed came out with the BTFP (or as Arthur calls it, “Buy the F*cking Pivot”).

BTC is now standing at a respectable $28,500, close to double from 2022 lows.

Based on my understanding, the BTFP doesn’t create or inject new dollars into the financial system, and thus shouldn’t be construed as QE redux. That said, I believe the broad market is rising on the changing waves of expectations, namely in interest rate hikes. Prior to the SVB / Credit Suisse crisis, markets were pricing >50% chance that Fed will hike 50bps and interest rates staying for most of 2024, but that reset to 25bps with numerous rate cuts expected in 2024.

Oh how things have changed…

Bitcoin and Ether have already appreciated (with haste) in just a week of trading, and continued further to the month-end. Talk about efficient markets. Even stock markets didn’t rise that quickly (in fact barely positive), which was why I felt that crypto benefitted from another narrative.

The narrative was what I had mentioned above - “Not your keys, not your coins”. While it was fortunate that depositors were made whole, the Fed or US Government will only do so, on the grounds that it would otherwise lead to systemic risk for the US financial system. This means that for other banks that could potentially suffer from future bank runs, their depositors are only insured up to 250K USD, which isn’t much from a business point of view. So, is your money really safe in banks?

In that sense, Bitcoin trumps all other ‘banks’ since you’re able to store value in a currency that only you yourself will own, and can transact freely with anybody in the world, separate from the fiat system. There won’t be a bank run since you’re free to convert your Bitcoin back into USD or any local currency.

Of course, there’s always the price risk, since Bitcoin, at the end of the day, is valued in US dollars. A bank run on Bitcoin will only lead to lower prices, as selling pressure increases. But more importantly:

1 Bitcoin will still be equal to 1 Bitcoin.

Arthur has an interesting article (Kaiseki) talking about this, if you’re interested.

I saw a long-form tweet from a crypto account that summarised the key events of 2022, which (if I’m honest), made the SVB crisis looked like peanuts. Crypto folk had suffered industry-level extinction events with Terra/UST, 3AC contagion, and the FTX fraud, amongst others, and here we are still standing and with 0 help from the government. If anything this highlights the resilience (Lindy?) of the industry, and so that alone is enough for me to continue investing in.

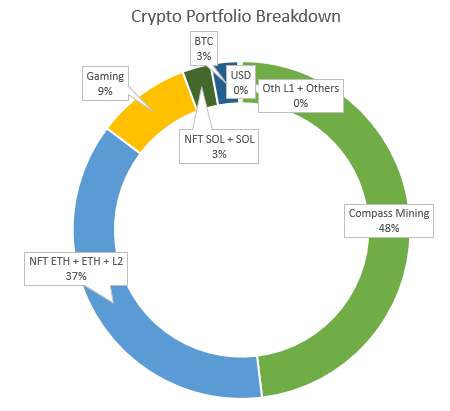

Portfolio

My portfolio holdings didn’t change much over the month, as I’m mostly fully invested. The main source of DCA is from my bitcoin miners, which nets me a small amount of Bitcoin per month.

It ain’t much, but it’s honest work.

It’s certainly not an ideal scenario, since mining bitcoin comes with operating costs, such as the facility fee, as well as the cost of the miner (which was a little too expensive when I bought it in 2021). Nothing much to complain about; one can only look forward and adapt.

As mentioned on-and-off in past months, my targets for crypto remains the same:

1-10 BTC

10-100 ETH

100-1000 SOL

These can include other coins within each ecosystem (so ETH can include ETH-based NFTs, or L2 tokens). Implicitly my target suggests that the preferred exchange rates for each token would be 0.1 BTC to 1 ETH, and 0.1 ETH to 1 SOL, or 0.1 BTC to 100 SOL. Let’s take a look at the prices now (end of Mar).

Both ETH and SOL has some ways to go in terms of catching up to BTC, which I think will be possible given their burgeoning (maxi?) ecosystem / community. Let’s review in 6 months, shall we?

My portfolio holdings below.

Compared to ETH and BTC, I felt like I had underperformed. Looking back, I think it is due to:

Depreciation for 8 of my miners (~1.8k USD),

Paying the facility / hosting fees for these 8 miners (~1.3k USD)

NFT prices wobbling a little from the prior month

Going forward, I shall focus less on crypto net worth, and more on the actual spot holdings (e.g. how many coins I hold). Since wealth is definitely not built in a day (or a month), we as long-term investors just need to stay the course, and understand what you’re investing in. It’s perfectly OK to underperform the majors in the short-term, but in the long-term one should, at the very least, outperform equity indices.

It’s a bumpy ride for sure, I’m enjoying every minute of it.

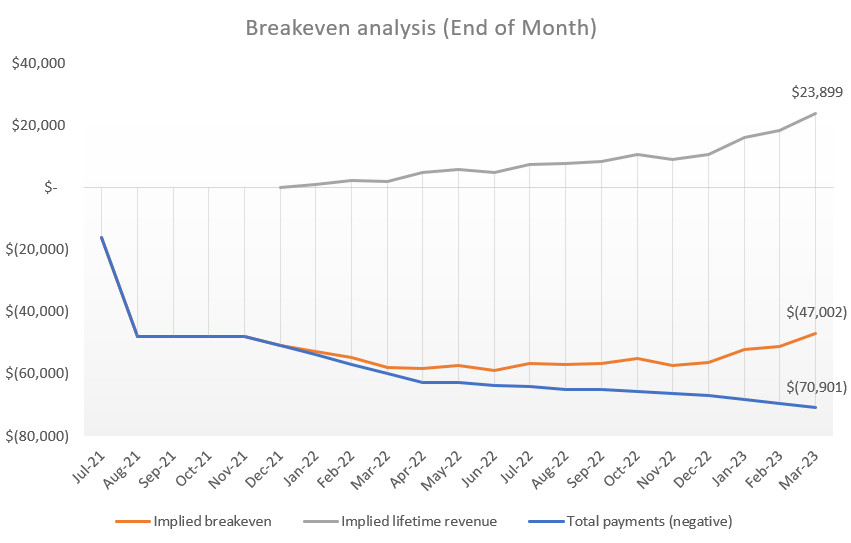

Mining

My mined Bitcoin benefitted from the appreciation in price, giving the impression that my mining operation is well on its way to breakeven. It’s not entirely true, because the implied breakeven assumes that you’ve kept all of the BTC that you mined.

I sold Bitcoin very generously over the past few months, into ETH, as well as into USD to fund my other altcoin purchases + facility costs. Going forward, I’ll probably have to be more stringent with my BTC sales, as I believe the bull market still has some legs to go. I might have to fork out money from my IRL bank accounts to fund this mining operation (instead of spare cash in my crypto wallets), but it is what it is.

Conclusion

Thank you for reading thus far. This edition is a little rushed, as I didn’t have much time at the end-of-month to make my thoughts more concise. That’s also why there wasn’t a “Life” section.

See you next month!

Cheers,

Joey